Table of Contents

Key Takeaways

- Average house prices in London across all property types stand at approximately £542,000 in March 2026 according to ONS data — down 2.1% year-on-year, with London’s headline figure masking enormous variation between boroughs, from £1,257,000 in Kensington and Chelsea to £364,000 in Barking and Dagenham.

- The most expensive London borough remains Kensington and Chelsea at £1,257,000 average — but prices there have fallen 7.5% year-on-year, the steepest drop of any borough, while cheaper outer boroughs such as Havering and Bexley have held broadly flat, narrowing the gap between the top and bottom of the market.

- Barking and Dagenham is the most affordable London borough for buyers, with an average of £364,000 in February 2026 — a borough that also now benefits from Elizabeth line access at Barking station, fundamentally reshaping its commuter proposition.

- Average house prices in London fell year-on-year in 19 of the capital’s 33 boroughs as of late 2025 — the correction is concentrated in prime central and prime inner London, while the most affordable outer boroughs have proved considerably more resilient.

- London’s average of £542,000 is more than double the UK national average of £268,000 — but first-time buyers in London are now targeting homes at an average of above £500,000 for the first time, according to Zoopla’s May 2026 House Price Index.

- The boroughs offering the strongest value relative to transport connectivity in 2026 are concentrated in outer east and south-east London — Barking and Dagenham, Havering, Bexley, and parts of Croydon — where Elizabeth line and mainline rail access delivers City and West End journey times that the headline price does not yet fully reflect.

Understanding Average House Prices in London

Average house prices in London are both the most cited and the most misleading statistic in British property. A single London average — whether £542,000 (ONS March 2026), £551,000 (ONS December 2025), or £666,000 (Land Registry twelve-month transactional average from April 2025 to March 2026) — tells a buyer very little about what they will actually encounter in the market. The variation between London’s 33 boroughs is so vast that averaging across them produces a figure that does not accurately represent the experience of buying in any of them.

What matters for any buyer is the specific average for the specific borough — and, within that, the specific neighbourhood, street, and property type they are targeting. This guide covers all 33 London boroughs, organised from most to least expensive, with the most current available ONS and Land Registry data, and the practical context that helps buyers use these figures meaningfully.

The two most authoritative sources for London borough price data are the ONS Local Housing Data, which provides monthly average prices by local authority using a hedonic regression model, and the UK House Price Index from HM Land Registry, which provides transaction-level data by postcode. Both are referenced throughout this guide.

The Most Expensive London Boroughs

1. Kensington and Chelsea — £1,257,000

The most expensive London borough and the most expensive local authority in England, Kensington and Chelsea has held the top position for decades. The borough encompasses Knightsbridge, Chelsea, Kensington, Holland Park, Notting Hill, and Portobello — some of the most globally recognised residential addresses in the world. The average of £1,257,000 in March 2026 represents a 7.5% fall year-on-year, the steepest correction of any London borough, reflecting the unwinding of prime central London values from their 2016 peak and the departure of some non-domiciled residents from the market. Despite the correction, it remains more than double London’s overall average.

2. City of Westminster — approximately £1,100,000–£1,150,000

Westminster encompasses Mayfair, Belgravia, St James’s, Pimlico, Marylebone, and the West End — a combination of prime residential and globally significant commercial real estate that sustains consistently high average values. The average private rent in Westminster stands at approximately £3,244 per month according to ONS data, the second highest of any London borough.

3. Camden — approximately £850,000–£950,000

Camden’s average fell 9.1% to approximately £778,000 in February 2026 on the ONS measure — though the borough’s wide range, from Hampstead’s Victorian villas to purpose-built flatted estates, makes any single average imprecise. The borough encompasses Hampstead, Belsize Park, Primrose Hill, Kentish Town, and the Bloomsbury academic quarter, each with its own distinct price profile.

4. Richmond upon Thames — approximately £850,000–£950,000

Richmond is the safest London borough by crime rate and consistently the highest-rated for quality of life. Its combination of Richmond Park, the Thames riverside, and direct Waterloo rail access sustains premium values. Average prices here have proved more resilient through the prime London correction than the inner boroughs.

5. Hammersmith and Fulham — approximately £800,000–£900,000

Hammersmith and Fulham encompasses Fulham, Brook Green, and Shepherd’s Bush — a borough that has consistently commanded a premium for its west London position, riverside character, and strong professional family buyer demand.

6. Wandsworth — approximately £700,000–£800,000

Wandsworth — covering Battersea, Clapham, Balham, Tooting, Putney, and Earlsfield — is one of the largest London boroughs by area and population, and one of the most actively traded property markets in south London. Battersea Power Station’s residential development has added significant new supply to the borough’s premium end.

7. Islington — approximately £679,000

Islington held 0.9% growth in the year to March 2026 — one of the few inner London boroughs to post positive annual growth — with an average of £679,000. The borough’s Zone 1 and Zone 2 transport access and the consistent demand from City workers have kept values supported through the wider London correction.

8. Hackney — approximately £596,000–£650,000

Hackney fell 3.7% to approximately £596,000 in February 2026, with flats — which account for around 78% of transactions — falling 4.4%. The borough has been one of the capital’s most dramatic gentrification stories of the past two decades, and despite the correction its values remain substantially above the London outer average.

9. Lambeth — approximately £580,000–£650,000

Lambeth encompasses Brixton, Clapham North, Streatham, Stockwell, and Herne Hill — a borough whose transformation from one of London’s most deprived to one of its most culturally energetic has been a defining narrative of the past twenty years. Brixton’s food and music scene anchors a diverse and active property market.

10. Southwark — approximately £570,000–£640,000

Southwark covers Bermondsey, Borough, Peckham, East Dulwich, and the Elephant and Castle regeneration area — one of the most geographically and demographically varied boroughs in London. The Elephant and Castle regeneration continues to reshape the borough’s central area significantly.

The Mid-Market Boroughs

Tower Hamlets — approximately £530,000–£570,000

Tower Hamlets encompasses Canary Wharf, Bethnal Green, Bow, Stepney, and Whitechapel — a borough defined by the contrast between the glass towers of the Docklands financial district and the historic East End communities of the surrounding streets. New build development around Canary Wharf has added substantial supply.

Haringey — approximately £530,000–£570,000

Haringey covers Muswell Hill, Crouch End, Hornsey, Tottenham, and Wood Green — a borough of substantial contrasts between its affluent northern hillside communities and the more affordable southern areas around Tottenham and Seven Sisters.

Merton — approximately £530,000–£560,000

Merton encompasses Wimbledon, Morden, Mitcham, and Raynes Park. Wimbledon’s combination of the All England Club, the Common, and Thameslink rail access sustains consistent premium values in the northern part of the borough, while the southern areas offer considerably more affordable options.

Greenwich — approximately £490,000–£530,000

Greenwich has benefited significantly from Elizabeth line connectivity at Woolwich, and the ongoing regeneration of the Woolwich Arsenal area has added new residential supply and commercial investment. The borough’s historic character — the Painted Hall, the Cutty Sark, the Royal Observatory — gives it a distinctive cultural identity.

Lewisham — approximately £440,000–£490,000

Lewisham covers Deptford, Lee, Forest Hill, Brockley, and Catford — a borough where gentrification has been working southward from the Deptford and Brockley end for a decade, and where the Overground and DLR connectivity has supported consistent buyer demand.

Ealing — approximately £490,000–£540,000

Ealing is one of the Elizabeth line’s primary beneficiaries — with multiple Elizabeth line stations across the borough (Ealing Broadway, West Ealing, Hanwell, Southall), journey times to the City and West End have been transformed. Southall has attracted particular attention as an undervalued market with strong Elizabeth line access.

Barnet — approximately £560,000–£610,000

Barnet is one of London’s largest boroughs, stretching from Whetstone and Finchley in the south to Barnet itself in the north. Its consistently strong school provision — including several outstanding secondary schools — makes it one of the most family-focused buying markets in outer north London.

Brent — approximately £450,000–£490,000

Brent covers Wembley, Harlesden, Kilburn, Brondesbury, and Queen’s Park — a borough that has seen significant price appreciation in its southern postcodes as buyers priced out of Islington and Camden seek Zone 2 alternatives.

Hounslow — approximately £450,000–£490,000

Hounslow’s position adjacent to Heathrow Airport and on both the Piccadilly line and District line makes it a practical and affordable base for the large workforce serving the aviation and logistics sectors. Chiswick at its eastern end is significantly more expensive than the borough average.

Harrow — approximately £480,000–£520,000

Harrow on the Hill’s distinctive hilltop character and the presence of Harrow School — one of England’s most celebrated independent schools — give the borough’s premium end a specific character. The wider borough serves a large and diverse population with Metropolitan line connectivity into the West End and City.

The Most Affordable London Boroughs

Croydon — approximately £380,000–£420,000

Croydon is the largest London borough by population and one of the most consistently cited as the capital’s best-value large outer borough. Thameslink services to Blackfriars, Farringdon, and St Pancras give it surprisingly strong City access for its price point, and the ongoing town centre regeneration — albeit delayed — is reshaping the commercial landscape.

Sutton — approximately £390,000–£430,000

Sutton is one of outer south London’s most family-friendly boroughs — strong state school provision, good road and rail connectivity, and predominantly suburban family housing stock at prices that represent genuine value by London standards.

Bromley — approximately £430,000–£470,000

Bromley is London’s largest borough by area, covering a wide range of settlement types from urban Crystal Palace and Beckenham to the semi-rural villages of the Bromley border country. Mainline rail access to London Bridge and Victoria makes it a practical south London family base.

Havering — approximately £390,000–£430,000

Havering in outer east London — covering Romford, Hornchurch, Upminster, and Rainham — is one of the most underappreciated value markets in London. Elizabeth line access at Romford and Harold Wood dramatically improves the central London commute from what were formerly considered remote east London addresses, at prices that are among the lowest available in any London borough.

Redbridge — approximately £430,000–£460,000

Redbridge benefits from Elizabeth line access at Ilford, and the combination of improved central London connectivity with a predominantly suburban housing stock of period semis and terraces makes it an increasingly competitive outer east London market.

Waltham Forest — approximately £430,000–£460,000

Waltham Forest has been one of London’s standout quality-of-life stories of recent years — Walthamstow’s market, wetlands, and creative scene have attracted consistent Sunday Times recognition alongside sustained buyer demand. The Victoria Line and Overground provide solid Zone 3 connectivity at prices that remain well below comparable Zone 2 addresses.

Enfield — approximately £390,000–£430,000

Enfield is outer north London’s most affordable significant borough, with good Great Northern rail access into Moorgate and Liverpool Street and a housing stock of predominantly interwar and post-war family houses at prices that compare favourably with closer-in equivalents.

Hillingdon — approximately £430,000–£460,000

Hillingdon is London’s second-largest borough by area, covering Uxbridge, Hayes, and the western fringes adjacent to Heathrow Airport. Elizabeth line access at Hayes & Harlington and West Drayton has improved central London connectivity significantly.

Bexley — approximately £380,000–£420,000

Bexley in outer south-east London offers Crossrail-adjacent value — Elizabeth line access is available from nearby stations — and a predominantly suburban housing stock of post-war semis and terraces at prices that are consistently among the lowest available in inner orbital London.

Newham — approximately £390,000–£430,000

Newham encompasses Stratford, West Ham, Forest Gate, and East Ham — a borough transformed by the 2012 Olympic legacy and by the combination of Elizabeth line, Jubilee line, DLR, and Overground services that make Stratford one of the best-connected transport hubs in London. Values here have not yet fully caught up with the infrastructure investment.

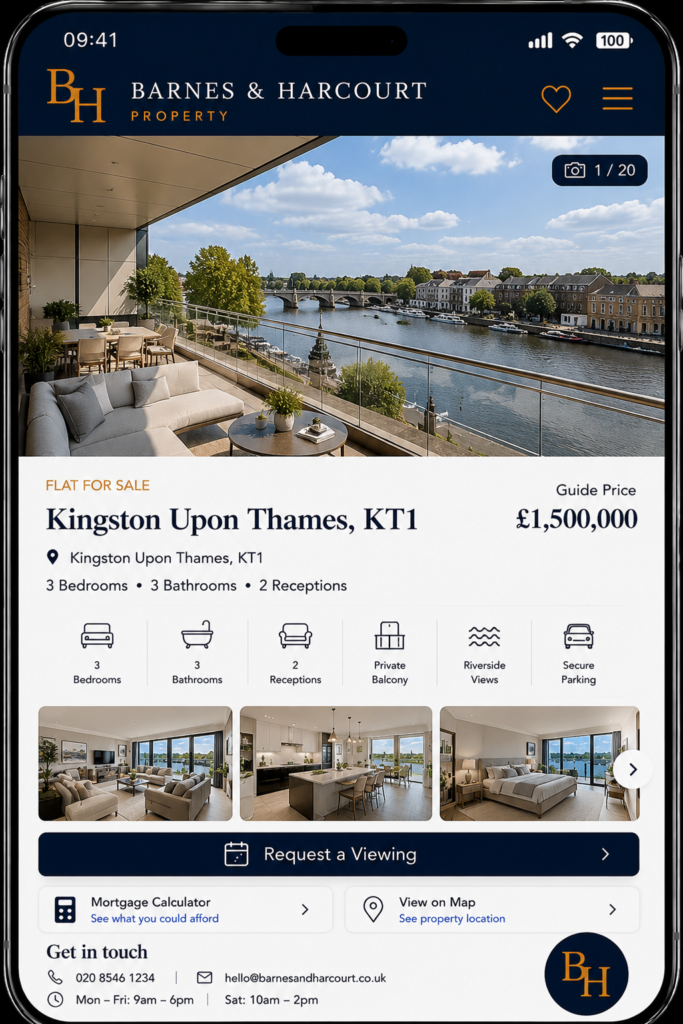

Kingston upon Thames — approximately £510,000–£550,000

Kingston is one of outer south-west London’s most practical and self-sufficient boroughs — a genuine town centre with department stores, good schools, and rail access to Waterloo at prices that remain well below the equivalent in Richmond or Wimbledon.

Barking and Dagenham — £364,000

The most affordable London borough in February 2026, with an average of £364,000 — Barking and Dagenham has consistently been London’s entry-level borough for buyers, and the arrival of Elizabeth line services at Barking station has added a central London connectivity dimension that fundamentally changes the value proposition. A buyer who could not previously justify Barking’s commute can now reach Bond Street in under 20 minutes.

What the Borough Price Data Tells Us About the 2026 Market

The Correction Is Concentrated at the Top

The most striking pattern in London’s 2026 borough price data is that the correction has been concentrated in the most expensive boroughs. Kensington and Chelsea is down 7.5%; Camden down 9.1%; Westminster and Hammersmith have recorded similar patterns. Meanwhile, the most affordable boroughs — Havering, Bexley, Barking and Dagenham, Croydon — have proved considerably more resilient, in some cases recording positive annual growth.

This pattern reflects the specific pressures on the prime central London market — the non-domiciled residency tax changes, SDLT surcharges on additional properties, and the departure of some international buyers — rather than any fundamental deterioration in London’s housing demand overall. At the affordable end, domestic buyer demand remains structurally strong.

The Elizabeth Line Has Reshaped the Outer Borough Value Map

The most significant structural shift in London’s borough price geography over the past three years has been the Elizabeth line’s impact on outer east London. Boroughs that were previously considered remote — Barking and Dagenham, Havering, Redbridge — now have journey times to central London that compare with historically more expensive Zone 2 and 3 addresses. This infrastructure effect is still working through the market, and buyers entering these boroughs in 2026 are acquiring a transport benefit whose full pricing impact has not yet been fully capitalised.

First-Time Buyers Are Being Pushed Further Out

The average price targeted by London first-time buyers has exceeded £500,000 for the first time according to Zoopla’s May 2026 data — a figure that effectively prices many first-time buyers out of the inner and middle ring of boroughs and pushes them toward the outer ring. This structural shift is one of the primary drivers of demand growth in the most affordable boroughs and reinforces the long-term case for outer London values relative to inner London alternatives.

Frequently Asked Questions

What is the average house price in London in 2026?

The average house price in London is approximately £542,000 in March 2026 according to ONS data — down 2.1% year-on-year. The twelve-month transactional average from the Land Registry puts the figure somewhat higher at approximately £666,000 across April 2025 to March 2026, reflecting a different calculation methodology. Both figures mask the enormous variation between boroughs — from £1,257,000 in Kensington and Chelsea to £364,000 in Barking and Dagenham.

Which London borough is the cheapest to buy in?

Barking and Dagenham is the most affordable London borough, with an average of £364,000 in February 2026 according to the Government’s UK House Price Index England report. This is followed closely by Bexley, Havering, Croydon, and Newham — all consistently among London’s most affordable boroughs and all with reasonable transport connectivity to central London employment centres.

Which London borough has seen the biggest price fall?

Camden recorded the steepest year-on-year fall at 9.1% to approximately £778,000 in February 2026. Kensington and Chelsea fell 7.5% to £1,257,000, and Westminster recorded similar significant falls. These corrections reflect specific pressures on the prime central London market rather than a broadly deteriorating London picture.

Which outer London boroughs offer the best value relative to transport?

Barking and Dagenham stands out — Elizabeth line access at Barking, average prices of £364,000, and central London journey times of under 30 minutes create a combination that is genuinely exceptional for the price. Havering (Romford Elizabeth line) and Bexley (southeast rail corridor) follow closely. In south London, Croydon’s Thameslink access to Blackfriars, Farringdon, and St Pancras provides City connectivity at prices well below most of inner south London.

Is London property still a good investment in 2026?

London’s long-term track record of house price growth above the national average is well established — though the past decade at the prime central end has been an exception to that pattern rather than a continuation of it. The structural case — population growth, housing undersupply, strong employment base, international appeal — remains intact. Analysts including Savills and Halifax forecast 2–4% growth for London through 2026, with outer boroughs likely outperforming the prime central correction. The key for any investor is borough-level rather than London-wide analysis, since the performance differential between boroughs has never been wider than it is in 2026.

Conclusion

Average house prices in London by borough in 2026 tell a story of a market in selective correction at the top and structural resilience at the bottom — a pattern that creates genuine opportunity for buyers who understand the geography rather than relying on the misleading London-wide average. Kensington and Chelsea’s £1,257,000 average and Barking and Dagenham’s £364,000 average both sit within the same city, served by the same transport network, and subject to the same national economic conditions. The gap between them defines the opportunity for the informed buyer who is prepared to look at the full borough picture rather than defaulting to reputation and received wisdom.

The ONS Local Housing Data and the UK House Price Index from HM Land Registry are the two most reliable sources for tracking these figures as they are updated monthly — essential tools for any buyer who wants to enter the London market in 2026 with objective, current, and granular data rather than the broad brush of a headline average.